With all of the attention on healthcare transparency, it seems ironic that Americans are more and more confused about healthcare, specifically their insurance policies. Continue reading “Healthcare Providers Must Educate on Patient Financial Responsibility”

Category: Industry News

Stay current on the latest industry news, best practices, and regulatory changes in revenue cycle management. Gain the knowledge you need to make informed decisions and drive successful outcomes for your healthcare organization.

Hot Topics in Healthcare: Increasing Revenue Cycle Complexities

If you think managing the healthcare revenue cycle is challenging now, brace yourself because there are several forces that are likely to drive more complication and complexity into the revenue cycle. Recent analyses of hospital finances are painting a complex picture – Medicare spending cuts, declining service volumes, rising costs, a shrinking payer mix, underutilized technology and increasing financial waste are all threatening the profitability of our hospitals and providers.

We’re Getting Older

As more and more baby boomers reach the age of 65, the mix of profit-generating commercial business and break-even to unprofitable government payers will continue to shrink. In addition to the increasing Medicare population, reductions in federal payments to hospitals will total $252.6 billion from 2010 to 2019, according to a new report commissioned by the American Hospital Association and the Federation of American Hospitals.

To compound the issue of an aging population and cuts in federal reimbursement, a report from Fitch Ratings predicts the third straight year of declining profitability for the nonprofit hospital sector, but not as steep as the previous two years. Finally some good news!

No More Passing the Buck

As the nation transitions from fee-for-service reimbursement to value-based care, coordinated efforts amongst an array of providers are required to improve quality and efficiency of patient care – and reimbursement. Under this approach, providers are financially rewarded for positive patient outcomes and efficient care delivery. This is a major shift in behavior from the traditional fee-for-service model, where providers are compensated for each test, treatment, and medication, regardless of patient impact.

While the goal of value-based reimbursement is expected to improve our population’s health, the shift in approaches brings along a new set of challenges for the healthcare industry. While many organizations are hiring care management coordinators and behavioral health support staff members to build the necessary infrastructure for value-based care, many are still citing the following as barriers to adopting this standard of care:

- Lack of staff time to collaborate between providers

- Unpredictability of revenue

- Lack of ability to understand potential financial risk

- Lack of resources to report, validate and use data

Regardless of these challenges, with only 39.1% of healthcare payments made in 2018 under a fee-for-service structure and the increased industry demand for value-based care, profitable provider organizations need to partner with each other and insurers to deliver value rather than passing the buck back and forth.

A Lot of Money is Wasted

Imagine throwing 25% of your paycheck right out the window. That is how much of healthcare spend in the United States is wasted. Administrative complexity is responsible for the most waste ($265.6 billion) – billing and coding errors and time spent reporting on quality measures. The authors of the report cited opportunities to reduce administrative waste through insurer-clinician collaboration and data interoperability.

The United States spends almost twice as much as other high-income countries on medical care despite similar utilization rates. Administrative costs were again identified as a major driver in the overall cost difference amongst the United States and other high-income countries.

The Data Struggle is Real

We are constantly surrounded by technology – from streaming TV, to an app that lets you see and speak to someone at your front door while you’re hundreds of miles away, to your Amazon packages being delivered by drones. There is no doubt that we are in the era of advanced technology, but adoption and investment in technology is still in its early growth stage in the healthcare industry. There could be several reasons why, including:

- A lack of general knowledge as to where to look for technology solutions

- A lack of understanding that there are solutions available to solve complex issues

- EHR implementations and maintenance is more challenging than anticipated

- All of the home-grown, legacy systems that require updating before being able to integrate with newer systems

Data interoperability is the key to these problems facing the healthcare industry. Being able to exchange, interpret, use and share data amongst other providers, payers and even the patients themselves would undoubtedly cut down on administrative waste and enhance the implementation of value-based care.

There is Hope!

These challenges are daunting, but the right partner can shed the necessary light and get your organization’s revenue cycle where it should be to maximize your revenue. Quadax is more than a revenue cycle management solution provider. We are in lockstep with our clients from the beginning and that service and commitment never ends. If you’re ready to learn how Quadax can help your organization support a growing Medicare population and a value-based care model while decreasing your administrative waste and making your data work for you, reach out any time!

Ken Magness is a focused healthcare professional with more than a decade of experience in helping clients understand the true value of automation in the revenue cycle management process. As the Strategic Initiatives Leader at Quadax, Ken and his team are passionate about connecting with healthcare providers to help them create and leverage the appropriate technology solutions to optimize the revenue cycle process and improve the experience of their patients and staff.

Ken Magness is a focused healthcare professional with more than a decade of experience in helping clients understand the true value of automation in the revenue cycle management process. As the Strategic Initiatives Leader at Quadax, Ken and his team are passionate about connecting with healthcare providers to help them create and leverage the appropriate technology solutions to optimize the revenue cycle process and improve the experience of their patients and staff.

Eliminating Medicare Denials is More Important than Ever!

With Election Day behind us and the upcoming Presidential election in 2020, Medicare for All is one hot topic. Continue reading “Eliminating Medicare Denials is More Important than Ever!”

A New Era of Consumerism Facing Labs Today – How Do You Stay Competitive?

By definition, consumerism is a social and economic order that encourages the acquisition of goods and services in ever-increasing amounts. Continue reading “A New Era of Consumerism Facing Labs Today – How Do You Stay Competitive?”

Hot Topics in RCM: Automation, Patient Experience and Analytics

We recently attended the American Association of Healthcare Administrative Management (AAHAM) Annual Conference in Las Vegas and brought home a wealth of insight… Continue reading “Hot Topics in RCM: Automation, Patient Experience and Analytics”

Surprise Billing Legislation: Ways to Mitigate Your Risk

Nearly 60% of insured adults have received a surprise bill on a healthcare service they thought was covered by insurance. And whether care or the provider is in-network, out-of-network or a mix of the two, 1 in 5 of these insured adults find it difficult to pay their deductibles.2 Why is this happening and what is being done about it?

Due in part to narrow provider networks, surprise bills can be the financial result of a patient receiving in-network care by an out-of-network provider, often the bill being the difference between the charged and the allowed amount of a service. These surprise bills can cause undue stress and have detrimental financial effects on the entire household, such as delayed payment on other household expenses, mounting credit card debt, and more. As such, state and federal legislations are responding in kind with laws around surprise bills.

STATE LEGISLATION

A number of states have enacted comprehensive laws to protect some patients from surprise medical bills, including California, Oregon, Illinois, Florida, New York, New Hampshire, New Jersey, Connecticut and Maryland. Additional states, including Texas, Colorado, New Mexico, and Washington, have passed laws expected to take effect this year. In essence, these laws are meant to protect consumers from surprise bills by limiting providers to the applicable in-network cost, setting a state payment standard, and/or establishing a dispute resolution process.3 Meanwhile, more than a dozen more states have enacted a limited approach to mitigate surprise bills.

FEDERAL LEGISLATION

Federal action is necessary to address certain aspects of surprise bills for people enrolled in self-funded plans due to the Employee Retirement Income Security Act of 1974, or ERISA. Legislation is expected to be passed in fall of 2019.

Both state and federal initiatives can be summed up as:

- All proposed legislation includes a ban on balance billing patients

- Most legislation is specific to emergency and ancillary providers at this time

- Many of the proposed state and federal bills include stipulations for using usual and customary rates as a basis for negotiation

- Arbitration clauses included in many of the proposed bills is considered favorable to providers

- Indexing against usual and customary rates seems to be included in more of the state initiatives

What can you do?

To help avoid and mitigate the risk of surprise bills, more and more hospitals and clinical laboratories are rethinking the patient experience and investing in tools to help provide pricing transparency on procedures and services, like testing. These tools utilize basic patient demographics (name, birthdate, address, insurance provider, etc.) to validate insurance coverage and eligibility, perform advanced benefit investigation to uncover plan-specific coverage details, assess prior authorization rules, and most importantly provide a patient’s expected out-of-pocket cost. Taking it even further, labs can identify a patient’s propensity and willingness to pay to help assess the need to offer financial assistance. This entire approach, called Patient Access Management, can help clinical labs and providers alike offer the transparency needed to empower a patient to make financial decisions regarding their care – perhaps the patient cannot afford the test so an alternative treatment plan has to be put into place. Patient Access helps to improve the patient experience in that the patient understands exactly what they will owe for the test – and no surprise bills. For a growing molecular lab, this can mean the difference between writing off bad debt and securing expected revenue.

To learn more about Patient Access Management solutions offered by Quadax and how they can help mitigate the risks of surprise bills and more, contact us today!

- http://www.norc.org/NewsEventsPublications/PressReleases/Pages/new-survey-reveals-57-percent-of-americans-have-been-surprised-by-a-medical-bill.aspx

- https://www.consolidatedcredit.org/infographics/medical-debt/#gref

- https://www.healthsystemtracker.org/brief/an-examination-of-surprise-medical-bills-and-proposals-to-protect-consumers-from-them/#

How does your zip code impact your health status?

Cleveland, home to Quadax headquarters, is also home to some of the finest medical facilities in the world. (Many of them, we’re proud to say, are Quadax clients.) At the same time, out of 88 counties in Ohio, Cuyahoga County (the greater Cleveland area) ranks 62nd for health outcomes[i]. Overall life expectancy is 1.6 years below the national average. Infant mortality is well above the national rate, with significant racial disparity. In terms of health factors contributing to outcomes, Cuyahoga County ranks 86th in Ohio for Physical Environment, and 81st for Social & Economic Factors, which include children in poverty, income inequality, unemployment, and violent crime.

In response to this dichotomy, Dr. Akram Boutros, M.D., FACHE, President and CEO of The MetroHealth System said, “It’s time to stop applauding medical care that’s administered after the fact, no matter how good it is, and start providing health care before people get sick.”[ii]

The MetroHealth System is doing just that, as announced in their recently-issued 2018 Annual Report, with the new Institute for Health, Opportunity, Partnership and Empowerment (H.O.P.E.)—just one of the programs they’ve created to identify and act on social determinants of health.

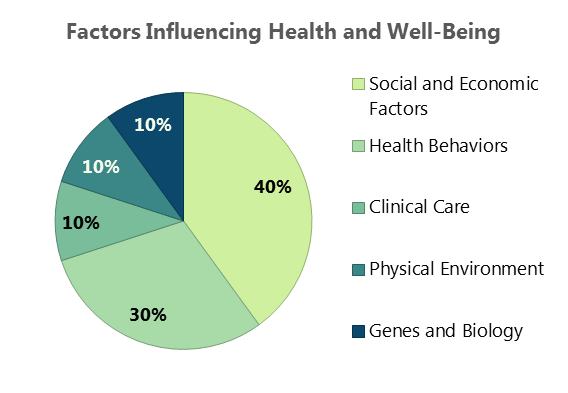

The Centers for Disease Control defines Social Determinants of Health (SDoH) as the conditions in the places where people live, learn, work, and play affecting a wide range of health risks and outcomes.[iii] “Right now in the United States of America in the year 2019, your zip code is more predictive of your health outcomes than your genetic code,” says Kate Walsh, President and CEO of the Boston Medical Center Health System. Commonly cited research reveals the contribution of clinical care to an individual’s health to be only about 10%, while socio-economic conditions, health behaviors, and physical environment combine to contribute 80% to a person’s health status.

Figure 1. Source: Minnesota Department of Health

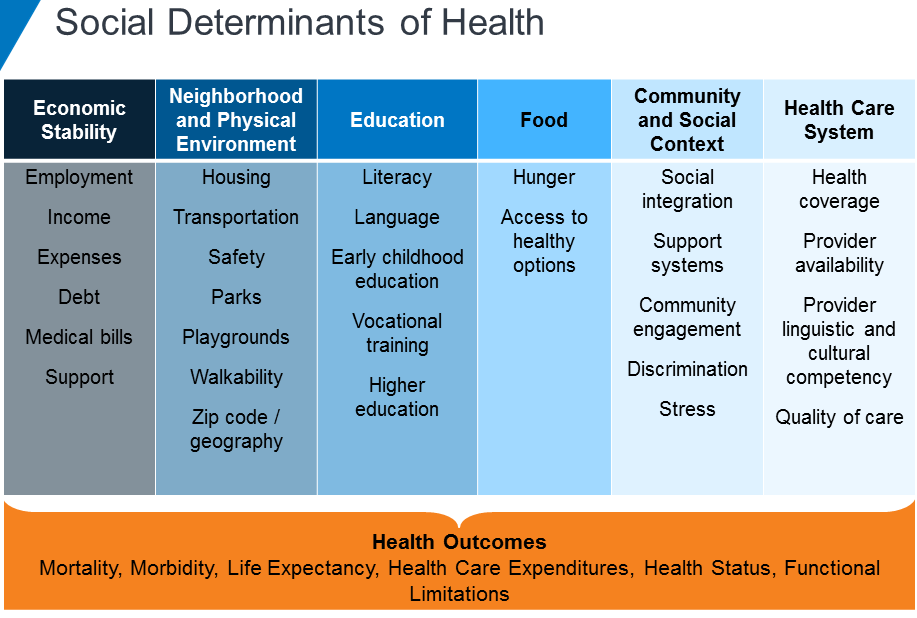

Lists of SDoH vary in number of categories, based on the arrangement of contributing factors, depending on the source. The CDC identifies five key areas; this table (below) from the Kaiser Family Foundation arranges the factors into six categories:

Figure 2. Source: Kaiser Family Foundation

The relationship between social conditions and health has been recognized for many years. Now, as our health care system shifts further toward value-based care, ever greater attention is being given to these socio-economic factors which will either support or undermine medical intervention.

AARP has found social isolation among older adults is associated with an additional $6.7 billion in Medicare spending annually. In people of all ages, factors such as social support, food security, economic stability, and physical safety will dictate their adherence to plans of care, making appointments, and avoiding hospital readmissions.

In a reimbursement environment focused on outcomes, providers will see greater success when patients’ health is established and maintained over the long term, enabling them to consume fewer acute care resources.

It’s a Community Thing

Dr. Boutros has stated, “Poor health doesn’t just affect the sick; it impacts entire communities.”He also observed, “The chronic stress of poverty has been demonstrated to hinder the development of executive function and to create dysregulation of emotion and attention. These lifelong effects are some of the underlying reasons why children living in poverty may not excel in school, choose risky behavior and have more suicide attempts.”

To that end, MetroHealth has developed programs to address Physical Environment, Health Behavior, and Socio-economic Factors in order to improve physical and mental health and reduce health care costs. The Institute for H.O.P.E will become a hub to provide access to resources and programs for education, employment, food, transportation, and housing. A grocery store, food pantry, classrooms, legal aid services, and financial literacy training are just some of the features planned. MetroHealth has also announced plans for new apartments, programs for employee assistance, and telemedicine service for college students in four states. These programs add to a long list of initiatives designed to transform the community, including the Open Table model.

A little less than two hours to the west of The MetroHealth System, ProMedica is likewise committed to caring for their community: the greater Toledo area, stretching into southeastern Michigan. In 2015, partnering with the AARP Foundation, ProMedica announced the formation of The Root Cause Coalition, a 501(c)(3) nonprofit organization to address hunger and other social determinants of health. In the same year, it opened its first food pharmacy, distributing food to patients with a physician referral. Since then, two additional Food Clinics have begun operation, and overall the Food Clinics have served more than 6,600 distinct households with “food as medicine.”

Recognizing many in ProMedica’s community live in food deserts, ProMedica has also invested in Market on the Green and a Mobile Market to bring fresh, local produce and fresh meat, dairy, and more at affordable prices to families and individuals who otherwise would never see fresh, healthful food in their neighborhoods.

According to Randy Oostra, President and CEO of ProMedica, “The healthcare industry must not only deliver clinical excellence and efficiency, we must hone in on how we can act as catalysts, innovators and leaders to improve the health of our entire communities.” Oostra has also observed that there is a business case for addressing social determinants of health in terms of lowering health care costs, reducing absenteeism, and increasing productivity.

Getting There from Here

In 2017, the Deloitte Center for Health Solutions conducted a survey of about 300 hospitals and health systems about health-related social needs investments. According to their findings, “80 percent of hospital respondents reported that leadership is committed to establishing and developing processes to systematically address social needs as part of clinical care.” However, current activity is often fragmented and ad hoc. There are gaps in screening, and finding sustainable funding is a challenge. Those hospitals making the greatest progress toward value-based care models, such as accountable care organizations (ACOs), are reporting the highest level of activity in the area of addressing social determinants of health.

Research into the association between social services coordination by health systems and a reduction in health care expenditures has to date been limited, but preliminary studies do show a positive correlation. A study conducted by WellCare Health Plans and the University of South Florida College of Public Health found a 10% reduction in health care costs for people who were successfully connected to social services for needs such as housing services and utility assistance.

Effective analysis of the return on investment for addressing social determinants of health requires hospitals employ data analytics to track meaningful measures—and to be patient as results are more likely to be seen over the long-term. Collecting data, selecting meaningful metrics, and understanding which components are providing the greatest ROI will depend on collaboration between clinical areas, social service partners, and revenue cycle representation.

While the data and analysis may take years to capture and understand, the data presently available on the connection between SDoH and health outcomes is clear and compelling.

As Dr. Boutros has pointed out, we have known for twenty years that increased Adverse Childhood Experiences lead to increased likelihood of diabetes, obesity, depression, sexually-transmitted disease, or suicide attempts. We also know, just as low-income Americans suffer higher rates of heart disease, diabetes, stroke, and other chronic conditions, poor health statuses also contribute to lower income, creating a cycle that’s hard to break.

Moving interventions upstream presents numerous challenges, but as characterized by Dr. Boutros, it’s a moral imperative.

Quadax applauds the efforts of The MetroHealth System and ProMedica in going beyond symptoms to tackle root causes and enhance the overall health of these Ohio communities.

In future articles, we’ll examine other SDoH initiatives as well as practical steps for moving forward with such efforts.

[i] https://www.countyhealthrankings.org/app/ohio/2019/rankings/cuyahoga/county/outcomes/overall/snapshot

[ii] Dr. Akram Boutros, “What Hospitals are Getting Wrong and How We Can Fix It,” delivered at The City Club of Cleveland, June 7, 2019. https://www.cityclub.org/forums/2019/06/07/what-hospitals-are-getting-wrong-and-how-we-can-fix-it Transcript here.

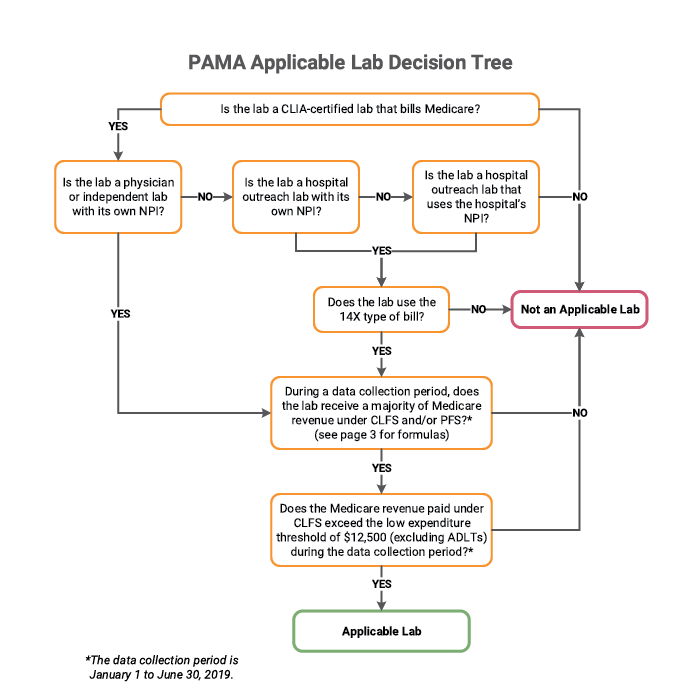

Is Your Lab Applicable Under the New PAMA Definition?

PAMA has already made a significant impact for hospital and independent labs, and continues to do so with the redefinition of an applicable lab. PAMA has expanded the number of reporting labs to include smaller labs and hospital outreach labs. CMS estimates at least 43% more labs are now required to report under the new definition. Therefore, labs not reporting during the first period need to double check their requirement.

As defined by CMS, an applicable lab is a laboratory receiving more than 50% of its total Medicare revenues from services paid under the CLFS or the physician fee schedule (PFS), with a low expenditure threshold. To meet the low expenditure threshold, a lab must have received $12,500 from final Medicare paid claims for services paid under the CLFS during the data collection period of January 1 to June 30, 2019.

A new wrinkle per the 2019 Final Rule is that Medicare Advantage revenues are excluded from the total Medicare revenue calculation. The change for round 2 that may have the greatest impact is that hospital outreach laboratories billing “non-patients” for laboratory services are now included in the applicable lab determination.

In Transmittal 3425, a non-patient is defined as a beneficiary who has a specimen that is submitted to a hospital for analysis but is not physically present at the hospital for the laboratory service; that is, the patient is neither a registered hospital outpatient nor an admitted hospital inpatient. Non-patients may be identified with the CMS-1450 14X TOB. An inherent challenge is that the 14X bill type is not necessarily used by commercial payers. This seemingly small modification will have significant impact to which organizations are considered “applicable labs” and to the algorithms by which providers select data for reporting.

Labs meeting these qualifications must then report “applicable information” to CMS. As a service to our clients, Quadax has developed the PAMA Applicable Lab Decision Tree shown below, which visually depicts the determination criteria.

Quadax financial reporting quickly and accurately provides the data needed to walk through this process and determine a lab’s status under PAMA. Quadax supports laboratories with tools to meet all regulatory requirements touching the revenue cycle. In addition to equipping labs with tools to help them identify their PAMA applicable lab status, Quadax makes it easy for applicable labs to select and segregate the correct, complete data required for submission.

To learn more, join us during this complimentary webinar, PAMA Tools & Strategies for The Next Round of Reporting on June 26, 2019 at 11:00 AM EDT.

This webinar will provide further insight into the strategies and tools successful labs use to determine applicable lab status, capture the appropriate claims population, and supply and normalize data to meet PAMA Reporting guidelines.

Steering Primary Care with Value-Based Reimbursement

Primary Care Physicians often feel they’re running out of gas. The value they provide is real: research shows significantly better healthcare access and experience for patients receiving primary care. However, office visits to primary care physicians (PCPs) declined 18% from 2012 to 2016[i], suggesting that the value of PCP care is not widely acknowledged. Meanwhile, physicians experience frustrations with administrative demands that encumber their ability to deliver needed care.

A JAMA Internal Medicine article reinforced the importance of primary care following a study of many thousands of US adults with and without primary care, concluding “policymakers and health system leaders seeking to improve value should consider increasing investment in primary care.”

Will the newly announced Primary Cares Initiative be the investment that makes a difference?

The American Academy of Family Physicians (AAFP) and America’s Physician Groups were among those applauding the CMS Primary Cares Initiative when it was announced on Monday, April 22.

AAFP Vice Speaker Russell Kohl, MD said, “To truly unleash the power of primary care, we must do two things: Unhinge it from the episodic-based incentives of fee-for-service, and eliminate the administrative complexity of practice that distracts family physicians from patient care. In short, it has become clear that we must create payment models that support our desired delivery models.”

Those distracting complexities cited by physicians in discussions of today’s greatest challenges include increased third-party administrative requirements, a rapidly changing reimbursement environment, and even measuring quality measure incentives and disincentives.

Time spent with EHR data entry is a significant frustration, as well. “EHRs were supposed to make patient records easily shareable among physicians. In theory, that would lead to more coordinated care and fewer medical errors,” says Sally Pipes, president, CEO, and Thomas W. Smith Fellow in Health Care Policy at the Pacific Research Institute in Forbes.

“Instead, the mandate has been a bureaucratic nightmare. Doctors now spend half their time on EHRs and desk work — and barely a quarter of their time with patients. In 2000, doctors spent more than 60% of their day providing medical care. The increasing bureaucratization of health care has left two in three doctors feeling burned out, depressed, or both.”

Enter the CMS Innovation Center and the Primary Cares Initiative, called “a major commitment advancing primary care in this country.” Health and Human Services Secretary Alex Azar introduced the new value-based care initiative in a speech at the Washington office of the American Medical Association.

The initiative comprises a set of five voluntary program models grouped into two paths: Primary Care First (PCF) and Direct Contracting (DC). PCF targets smaller practices, offering a general payment model and a second payment model for high-need populations. The three models in the DC path are Global, Professional, and Geographic; these target larger practices and are more ambitious.

The payment models incentivize participating providers to deliver advanced, patient-centered primary care services while keeping those patients healthy and out of the hospital. They focus on value-driven, population-based metrics.

In the PCF general model, population-based payments and flat primary care visit fees are meant to assist in the transition from fee-for-service to a value-based model. Performance-based adjustments can reward providers up to 50% of revenue, or risk a 10% downside adjustment. Quality measures include acute hospital utilization in all 5 years of the program; starting in year 2, quality measures will include Patient Experience of Care Survey, control of hemoglobin A1c and hypertension, care plan, and colorectal screening. The Quality Gateway for practices serving high-risk and seriously ill populations will be developed during the model.

Data sharing is a key component of the program. The plan for PCF data sharing is for participants to submit claims (with reduced documentation requirements) to CMS, and for CMS to return performance data to providers, to be used in their own analytic tools, so that providers may assess their own and their peers’ performance in the program to encourage continuous improvement.

Administrator Verma, in remarks to the National Association of Accountable Care Organizations, said, “Technology, and the sharing of data, underpin the entire move to innovative payment mechanisms. Without effective, open data sharing, providers cannot keep patients healthy. Without data to track patient progress or understand quality, payers cannot tie payment to outcomes.” To this end, CMS is moving to modernize their processes for data sharing, encouraging APIs wherever possible. The intent is for providers to “track their beneficiaries’ healthcare utilization and spending at a granular level, and then modify a patient’s care plan in response.”

The vision for value-based care is to both hold clinicians accountable for cost and quality while also giving them the flexibility to innovate—to provide quality, coordinated, appropriate care free from the dictates of bureaucracy and regulation. Azar referenced the 4 Ps that are the goals of value-based care according to CMS:

- Patients in control as consumers

- Providers acting as accountable guides through the healthcare system

- Payments based on outcomes

- Preventing disease before it occurs or progresses

It’s not clear whether value-based payment models will automatically result in a complete system of value-based care delivery, though such an outcome would be good for both patients and physicians. Reimbursement has been recognized as an effective steering wheel for the vehicle of healthcare delivery, however, so there is optimism for the results of this and subsequent initiatives. Further, by encouraging multi-payer alignment, CMS hopes to retain firm control of the steering wheel.

Administrator Verma has indicated additional value-based payment models will be forthcoming, including programs for rural care, oncology, and other specialty physicians and surgeons. She has also said future models are likely to be mandatory rather than voluntary.

For the Primary Cares Initiative, participation is voluntary, and several conditions must be met in order to apply for the program. The application process is expected to begin soon—“Spring 2019” according to the CMS timeline. Qualifications for participation in PCF include geographic and demographic aspects, having experience with other value-based payment arrangements, using 2015 Edition Certified Electronic Health Record Technology (CEHRT), supporting data exchange with other providers and health systems via Application Programming Interface (API), and connecting to their regional health information exchange (HIE). Practices must also comply with a set of “advanced primary care delivery capabilities,” such as providing 24/7 access for patients to practitioners.

What does this mean for the business office?

Under a payment model such as PCF, claim processing will be different, but still vital. Hopefully, rejections and denials will be minimal, but it is unlikely payment discrepancies will disappear. Nor will the revenue cycle functions of patient access management, coding, cash application, etc. be rendered either inconsequential or obsolete.

Data tracking and analysis will become more important than ever to practices as they evaluate performance, innovate based on outcomes, and predict and confirm performance-based adjustments.

Data preparedness is associated with disaster readiness and response; it’s the “ability of organizations to…effectively deploy and manage data collection and analysis tools, techniques, and strategies in a specific operational context.”[ii] In the context of value-based payment, data preparedness and ease with analytics capabilities is important for providers prior to joining a model, in order to confidently assume risk. Understand your patient population, have a clear picture of costs and budgeting, and be ready to work with payment and performance data following model implementation.

Many unknowns remain as we look to the future of healthcare reimbursement—of course, that’s nothing new. What is known: the best way to succeed regardless of payment model (or variety of them) is to ensure all the parts of your revenue cycle are operating at peak efficiency. When your staff enjoys greater productivity with cost-effective, connected tools for patient access, claims management, reimbursement management, and data analytics, you’ll be ready to hit the value-based road with confidence.

Quadax can help. Contact us to hear how we’ve helped both primary and specialty physician groups optimize their workflow and their cash flow.

To learn more about each path under the Primary Cares Initiative, tune in to an upcoming CMS webinar: for Primary Care First or for Direct Contracting.

[i] Health Care Cost Institute, HCCI Brief: Trends in Primary Care Visits, October 2018 https://www.healthcostinstitute.org/research/publications/hcci-research/entry/trends-in-primary-care-visits

[ii] Nathaniel Raymond and Ziad Al Achkar, Data preparedness: connecting data, decision-making and humanitarian response, November 2016 https://hhi.harvard.edu/publications/data-preparedness-connecting-data-decision-making-and-humanitarian-response

Quadax Earns Top Honors Again as KLAS Category Leader for Claims Management

CLEVELAND, January 31, 2019 – Quadax, Inc. was named Category Leader for Claims Management for the second year in a row in the 2019 Best in KLAS: Software & Services report, which names the top-performing vendors that help healthcare professionals provide better patient care.

Ultimately this rating was earned because of the interviews KLAS conducted with users of the Quadax Claims Management application, Xpeditor. Unanimously, our clients agree Xpeditor™ helps healthcare organizations expedite payments and reduce the cost and effort of managing claims. The Quadax library of standard edits is so comprehensive, nearly all Xpeditor claims are accepted by payers on the first pass.

In addition to great technology, Quadax leads the industry because of our exceptional service and support model – responsive, timely and proactive to our clients’ unique needs. While many in healthcare tend to think of claims processing as a commodity, Quadax continues to demonstrate providers can and should expect more from their claims management vendors.

Tony Petras, COO, EDI Services, stated, “We are gratified to know our clients consider our performance worth sharing with KLAS Research. We will continue to work to raise the bar throughout 2019 and the years to come, as we engineer better ways to serve our clients and help them continually produce better results.”

Quadax empowers clients to drive costs out of the healthcare revenue cycle. With solutions for patient access, claims, reimbursement, denials, appeals & audit management, plus business analytics, our efficient, highly configurable system for claims submission and tracking transforms operations and puts our clients in control.

KLAS data is freely available to healthcare providers. You can learn more about KLAS and the insights they provide, and download the 2019 Best in KLAS: Software & Services Report.

About Quadax, Inc.

Quadax is a healthcare services and information technology company focused on making the business of healthcare run better. The company partners with payers, hospitals, physician offices, laboratories and others to allow them to focus on their role in providing quality healthcare. Quadax improves clients’ financial and operational performance with innovative solutions, strategies, and services built on superior software technologies that include accounts receivable systems, revenue cycle management services, electronic transaction management systems, and reimbursement support services. To learn more, visit us at www.quadax.com or follow us on LinkedIn or Twitter.