Keeping you in the know on the constantly changing world of medical billing and reimbursement, Quadax compiles industry news and articles covering important billing-related topics and issues.

Category: Industry News

Stay current on the latest industry news, best practices, and regulatory changes in revenue cycle management. Gain the knowledge you need to make informed decisions and drive successful outcomes for your healthcare organization.

Considerations for Private Companies Implementing ASC 606 Revenue Guidance – Part 2

Part 2: Audit Requirements

To assist private companies in understanding what the auditors will request and review, we have identified some of the relevant auditing standard requirements below.

Management’s implementation plan and documentation

Management’s implementation plan encompasses many activities—scoping, accounting assessment, solutions development, and other activities. Auditors need obtain an understanding of this plan.

From a scoping perspective, management is expected to have a variety of key processes and controls implemented to identify revenue streams, relevant contract components and features and business practices to support their accounting policy conclusions. Auditors need to understand how management selected contracts to validate the contract components and features identified during the initial scoping phase. Auditors will also need to perform testing to validate management’s assessment in order to provide support to the audit opinion.

From an accounting assessment perspective, the auditing standards require the auditor to obtain an understanding of the entity’s accounting policies including the reasons for any changes in these policies. To do so, auditors will be reviewing management’s documentation to determine if the accounting policies comply with ASC 606, and validating that the company’s accounting complies with those policies.

Internal control considerations

The auditing standards require the auditor to obtain an understanding of company’s internal controls relevant to the audit. Further, the auditor must evaluate the design of the controls and determine whether they have been implemented by performing procedures in addition to inquiry of the entity’s personnel. As a result, management must evaluate how any changes due to the implementation of ASC 606 impact its control environment.

Further, the new guidance requires management to either recast prior-period financial statements presented for comparative purposes (full retrospective method) or record a transition adjustment and provide disclosures of significant changes by financial statement line item (modified retrospective method). Management must have controls and processes in place for either method chosen. Auditors must obtain an understanding of those controls and test to substantiate there is not a material misstatement.

Extensive new disclosures

The extensive new disclosures required by ASC 606 may require companies to update systems, processes, and controls used to develop disclosures. It is important to note that those companies that assert they will experience little or no impact to top line revenue due to adopting ASC 606 will likely still expend a significant amount of effort to comply with the extensive new disclosure requirements. The auditors will need to perform testing in order to substantiate the new disclosures and underlying information used to support those disclosures.

Management’s progress

It is important for companies to keep their auditors abreast of implementation issues and progress. The more communication the company and auditors have throughout the implementation process, the less likely it is that surprises will arise.

The following indicators may lead the auditor to conclude that management is behind or failing to execute their implementation plan and, therefore, may necessitate additional work:

-

-

- Inability of management to articulate the details of their implementation plan or make progress toward implementing that plan

- Lack of a detailed implementation plan and timeline

- Evidence that key deadlines from the timeline have been missed and that there are neither plans to catch up nor enough time to do so

- Poor tone at the top, including lack of involvement from those charged with governance

-

Where do we start?

A comprehensive implementation plan that includes the right people across the right functions is critical to a successful implementation of the new guidance. Companies should consider the following action items as they tackle ASC 606:

-

-

- Train employees across the organization on ASC 606, and allow employees to help identify impacts to their own functional areas (forecasting, employee benefits, tax, sales teams)

- Develop an overall implementation plan and timeline

- Evaluate competence across the organization, and consider hiring external service providers to assist with the implementation process, as needed

- Inventory all contracts with customers and identify key terms and conditions, as well as any deviations from those standard terms

- For areas of change between existing GAAP and ASC 606, identify cross-functional impacts to the organization (including tax impacts)

- Make any accounting policy elections and document new policies, as needed

- Document and implement any internal control changes

- Identify disclosure gaps that require system updates or changes, and initiate the process to close those gaps

-

“One of the biggest takeaways we hear from public companies is not to underestimate the amount of time required to complete the implementation of ASC 606. Because the new guidance touches so many areas of the business, the implementation requires extensive coordination across functional areas which, of course, takes time and effort.”

Cullen Walsh, Partner

Grant Thornton Accounting Advisory Services

Want to learn more about how ASC 606 can affect your organization? Join Cullen Walsh, Partner, Accounting Advisory Services at Grant Thornton and Walt Williams, Director of Revenue Optimization and Strategy at Quadax, as they present, “ASC 606 – Lessons Learned and What You Need to Know” on Tuesday, November 27 at 2:00 p.m. EST.

Register For Webinar

For more information on how Grant Thornton can help your company, contact your GT Audit Partner Daryl Buck, Cullen Walsh, Matthew McCleary, Chris Stephenson, or your local GT service provider.

“Grant Thornton” refers to Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd (GTIL), and/or refers to the brand under which the GTIL member firms provide audit, tax and advisory services to their clients, as the context requires. GTIL and each of its member firms are separate legal entities and are not a worldwide partnership. GTIL does not provide services to clients. Services are delivered by the member firms in their respective countries. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or omissions. In the United States, visit grantthornton.com for details.

© 2018 Grant Thornton LLP. All rights reserved. U.S. member firm of Grant Thornton International Ltd

Considerations for Private Companies Implementing ASC 606 Revenue Guidance – Part 1

By: Grant Thornton LLP (Special Guest Post)

As the effective date for the new revenue guidance in ASC 606, Revenue from Contracts with Customers, quickly approaches for many private companies (January 1, 2019 for calendar-year companies), management and audit committee members are faced with many questions.

- What lessons have been learned from public companies’ implementation of the new revenue standard?

- What will my auditor be looking for?

- Where do we start?

This blog addresses these questions and serves as a conversation prompter to help executive management engage with those parties involved in the implementation process.

Remember, implementing the new revenue guidance is not just an accounting exercise. The implementation process is a cross-functional exercise that requires coordination between tax, sales, and information technology (IT), among other functions.

“Even companies that are not expecting a material change in revenue must undergo an exercise to identify gaps between existing accounting and ASC 606, determine if any changes need to be made (including system changes), implement the changes, and document the analysis for the external auditors. This process can be time-consuming and require significant effort.”

Daryl Buck, National Managing Partner

Accounting Advisory Services

What lessons have been learned?

As public companies are in the process of finalizing their ASC606 implementations, we can share some “lessons learned” from observing the implementation process and interviewing those overseeing the implementation process.

Get the right people involved, earlier rather than later

Because of the pervasive effect of the new guidance on an organization, management must identify the right stakeholders to provide input into the implementation process. Not only does a company need to identify the right people within the organization to provide input (sales teams, IT, tax), but a company should not hesitate to engage external professionals where assistance is needed (training, technical accounting expertise, IT changes, etc.). Getting the right team in place from the start is key to a successful implementation.

Do not underestimate the effort required to inventory contracts

One of the first implementation tasks for many companies is to inventory their existing revenue contracts, identify standard terms and conditions, then determine if any contracts deviate from those standard terms. For companies that allow sales teams to deviate from standard contract wording, this process can be time consuming and require extensive communication and coordination.

Allow extra time for key contract terms

The new revenue guidance requires companies to evaluate their existing arrangements against the new five-step revenue model. This analysis may be straightforward for some contracts, but if your contracts include any of the following provisions, plan to spend extra effort and time to address these provisions and document your analysis:

1. Multiple goods or services — Performance obligations are the unit of account for applying the new revenue standard, so determining the appropriate performance obligations in a contract is critical to how a company will recognize revenue. The criteria for identifying performance obligations are new and therefore companies need to take a fresh look at their goods and services and assess them against the new criteria.

2. Variable consideration (meaning any consideration that causes the transaction price to vary) such as retrospective volume discounts, rebates, bonuses, or penalties — The new revenue standard generally requires companies to estimate these amounts for purposes of determining the transaction price and evaluate whether to constrain the amount of estimated variable consideration to ensure that revenue is recognized only to the extent it is probable that a significant reversal in cumulative revenue recognized for the contract will not occur when the uncertainty is resolved.

3. Material rights (for example, a prospective volume discount that is incremental to the range of discounts typically given to a particular class of customer in a geographical area or market) — Under the new model, a company must account for a material right as a separate performance obligation and this may require a complex accounting exercise to allocate a portion of the overall transaction price to the material right performance obligation.

4. Modifications — ASC 606 includes prescriptive new guidance for modifications and this has necessitated some companies to implement system solutions to track and account for these modifications.

5. Contract costs — The new revenue standard introduces guidance for costs incurred from a contract with a customer, which has been codified in ASC 340-40. Companies are required to capitalize certain costs under this new guidance and therefore companies that may have elected to expense certain costs in the past may experience a change under the new guidance.

6. Customized goods — Companies that produce customized goods and have an enforceable right to payment for work completed to date may experience a change in accounting as the new guidance requires the company to recognize revenue as it performs the work, that is, over time (rather than at a point in time).

Do not forget about disclosures

Private companies may be spared from some of the new, extensive disclosure requirements that public companies have to comply with, but private company disclosures will still require significant time and effort. Private companies must disclose disaggregated revenue information, information about performance obligations, and significant judgments in determining the timing of satisfying performance obligations and in estimating variable consideration.

Watch for Part 2 of this blog series addressing audit requirements and considerations on November 13.

Want to learn more about how ASC 606 can affect your organization? Join Cullen Walsh, Partner, Accounting Advisory Services at Grant Thornton and Walt Williams, Director of Revenue Optimization and Strategy at Quadax, as they present, “ASC 606 – Lessons Learned and What You Need to Know” on Tuesday, November 27 at 2:00 p.m. EST.

Register For Webinar

For more information on how Grant Thornton can help your company, contact your GT Audit Partner Daryl Buck, Cullen Walsh, Matthew McCleary, Chris Stephenson, or your local GT service provider.

“Grant Thornton” refers to Grant Thornton LLP, the U.S. member firm of Grant Thornton International Ltd (GTIL), and/or refers to the brand under which the GTIL member firms provide audit, tax and advisory services to their clients, as the context requires. GTIL and each of its member firms are separate legal entities and are not a worldwide partnership. GTIL does not provide services to clients. Services are delivered by the member firms in their respective countries. GTIL and its member firms are not agents of, and do not obligate, one another and are not liable for one another’s acts or omissions. In the United States, visit grantthornton.com for details.

© 2018 Grant Thornton LLP. All rights reserved. U.S. member firm of Grant Thornton International Ltd

Hanging in the Balance: Addressing Surprise Billing Issues

The topic of balance billing is in the news again, closely associated with the newer term, “surprise billing.” Patient experiences such as those of Drew Calver, who received an unexpected $109K bill following treatment for his heart attack, have focused new attention on this long-standing issue.

Balance billing is the practice of pursuing from the patient any balance remaining on account after the insurance payer has reimbursed its portion to the provider, beyond the expected co-pay, co-insurance, and deductible. The terms of the contract between the provider and insurance plan will generally dictate what is or is not billable to the patient – the aforementioned co-pay, co-insurance, deductibles, for example – and these contract provisions (and state law, typically) will control whether or not a patient may have further financial responsibility.

When there is no contract, of course, all bets are off, since an out-of-network provider has no negotiated payment rate. As high-deductible health plans have become more widespread, many patients are keenly aware of the benefits of staying in-network to keep those expected costs as affordable as possible. But what about when services must be rendered by an out-of-network provider?

In a number of cases highlighted by the media recently, a patient was not aware that out-of-network providers were engaged in the treatment. This commonly happens when an emergency department physician working through a staffing agency, or an anesthesiologist or radiologist is involved in care but is not in-network. Hence, the surprise of “surprise billing” – the receipt of an out-of-network bill when the patient thought they were at an in-network facility.

New Jersey’s Assembly Bill No. 2039 has likewise garnered quite a bit of attention since its enactment and particularly since its effective date August 30, 2018. Governor Phil Murphy, who signed the legislation earlier this year, said “We’re closing the loophole and reining in excessive out-of-network costs to prevent residents from receiving that ‘big surprise’ in their mailbox. At the same time, we’re making healthcare more affordable by ensuring these costs are not transferred to consumers through increased health premiums.”

New Jersey is among 21 states that have partial or comprehensive protections against balance billing by out-of-network providers in emergency departments or in-network hospitals. Stipulations of the protections vary by state. Variables include applicability by setting, type of managed care plan, the type of protection, and the payment outcome, whether a payment standard or a dispute resolution process. And since ERISA currently exempts self-funded employer sponsored plans from state regulation, 61% of privately insured individuals are not covered by their state’s protections, adding to the complexity.

There is speculation that changes could be made to ERISA (the Employee Retirement Income Security Act of 1974) to overcome this loophole to state protections. Senator Bill Cassidy, M.D. (R-LA) announced on September 17 a discussion draft of a bill that would modify ERISA to defer to state limits for patient costs for emergency care; or, in absence of state limits, define restrictions within the proposed legislation itself to cap patient responsibility. This is one issue among several concerning healthcare price transparency that is being discussed by a working group, and not the only discussion on the topic of potential laws governing balance billing.

So what’s a healthcare provider to do?

- Be aware of the regulations applicable in your state, and be prepared to comply. As media focus continues on this topic, more legislators are taking up the issue. Stay tuned to your state’s law-making process to eliminate surprises for your cash flow.

- Apply your organization’s payment policies consistently.

- Communicate clearly with patients, whenever possible, about the charges they should expect and their options for payment. In non-emergency settings, check patient eligibility, and provide a pre-service estimate based on their health plan coverage.

Complex billing issues are par for the course in today’s healthcare business office. That’s why Quadax delivers software and solutions that solve revenue cycle complexities, streamlining accounts receivable and reimbursement operations to improve cash flow and payment results.

If you’re ready to work with a partner that believes in transparency, communication, and earning our clients’ trust every day, get in touch with Quadax!

Quadax Earns KLAS Top Ranking for Claims Management

The Secret is Out!

With the release of the 2018 Best in KLAS: Software and Services report, the healthcare industry is learning what Quadax clients have known for years: Quadax can’t be beat for exceptional service and top-performing product functionality.

Although Quadax has served hospitals, laboratories, physician groups, and many others in the healthcare industry for more than 40 years, we have done so somewhat quietly. “Quadax is the industry’s best kept secret; a small but mighty company with talent and expertise to help all types of providers,” said Terry Buterbaugh, Senior Software Engineer.

Instead of making a lot of noise, we’ve focused our attention on building partnership with our clients. We continuously work to improve our revenue cycle products and services to meet the needs of providers looking for high-performing transaction management tools to improve operational efficiency and cash flow, cost-effectively.

Quadax Performance

You expect comprehensive standard edits for cleaner claims and faster payments, and Quadax delivers. Thanks to the diligence of our team of claim edit researchers, 99.6% of the claims we transmit are accepted by payers on the first pass. The Quadax Claims Management system, Xpeditor, also gives you powerful tools for configuration of custom edits and claim data processing rules as well as dynamic workflow rules to fit your business office. Not the other way around.

Inseparable from our superior products are the people of Quadax EDI Services that empower providers to use the Xpeditor system to its fullest by providing person-to-person, relational customer support. Whether it’s on-site, on the phone, through virtual meetings, or otherwise—we’re here for you.

Quadax is honored to receive the distinction of Category Leader for Claims Management. However, the driving force behind all that we do is not the achievement of a trophy or seal. Rather, it’s the attainment of a relationship of trust and mutual benefit with the healthcare providers we serve. We enjoy overcoming new challenges as they arise, rolling up our sleeves, and working with client teams to help them achieve success.

If the power and flexibility of Xpeditor are news to you, we’d love to let you in on the secret. Contact us so we can give you more information and show you what makes Quadax Claims Management #1!

KLAS Research

KLAS is a data-driven company on a mission to improve the world’s healthcare by enabling provider and payer voices to be heard and counted. Working with thousands of healthcare professionals, KLAS collects insights on software, services and medical equipment to deliver reports, trending data and statistical overviews. KLAS data is accurate, honest and impartial. The research directly reflects the voice of healthcare professionals and acts as a catalyst for improving vendor performance.

Each year, KLAS publishes a Best in KLAS Report, identifying the top vendors in more than 80 categories. “Category Leader is more than a ranking. It is a recognition of vendors committed to delivering superior solutions,” said Adam Gale, President of KLAS. “It gives voice to thousands of providers who are demanding better performance, usability and interoperability in healthcare technology.”

The Best in KLAS Report scores vendors on the performance categories sales and contracting, implementation and training, functionality and upgrades, service and support, and general. What they learned put Quadax at the top of the list.

KLAS data is freely available to healthcare providers on their website. You can learn more about KLAS and the insights they provide, and download the 2018 Best in KLAS: Software & Services Report when you log in or create a free account.

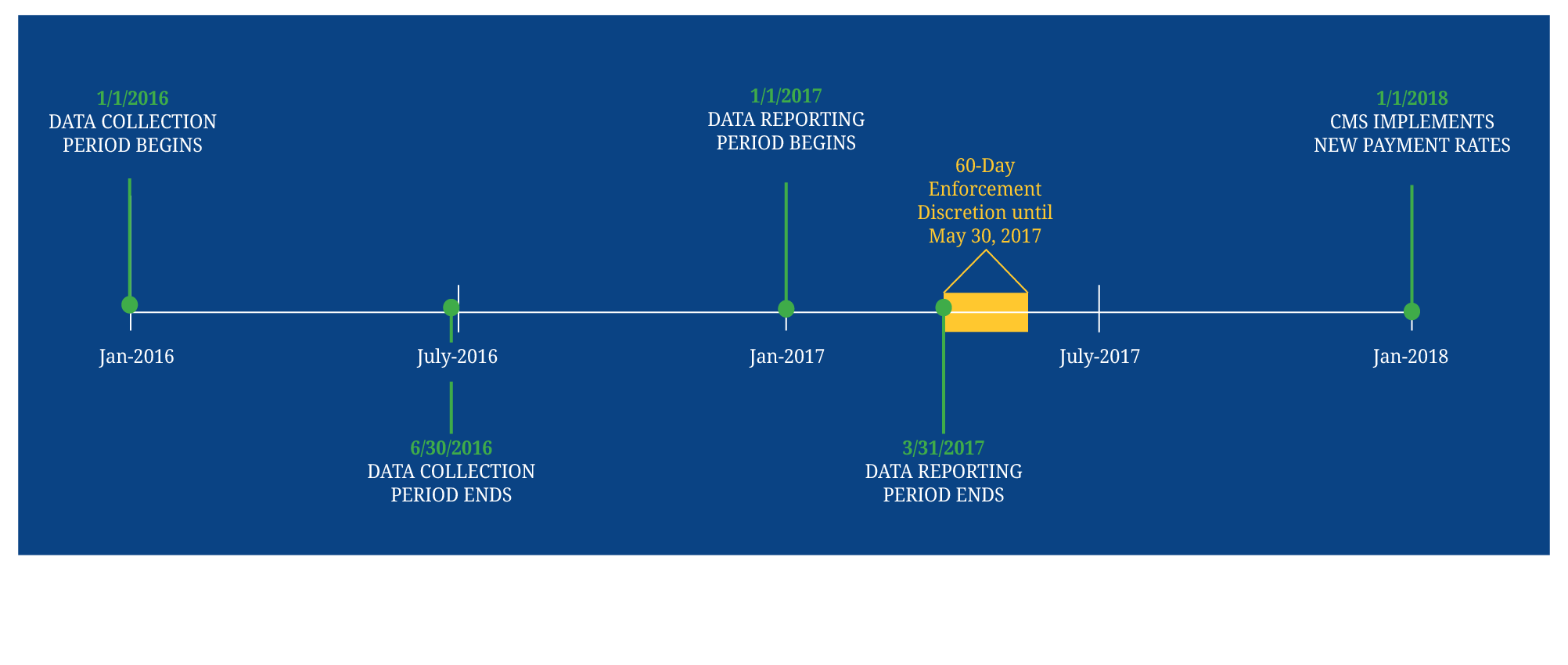

OPPS 2018 Revisions: Outpatient 14-Day Rule Changes to Laboratory DOS Policy

Centers for Medicare and Medicaid Services (CMS) published its final rule with comment period revising the Medicare Hospital Outpatient Prospective Payment System (OPPS) for 2018. Labs that provide services to hospital outpatients may want to review the new OPPS rule changes, particularly the revisions to the laboratory date of service (DOS) policy (see CMS excerpt highlighted below).

The new carve out exceptions to the 14-day rule will allow labs to bill Medicare directly under the Clinical Laboratory Fee Schedule (CLFS) for molecular pathology tests and advanced diagnostic laboratory tests (ADLTs) that are excluded from OPPS packaging rules and ordered less than 14 days after a patient’s outpatient hospital discharge. In these instances, the DOS for the excepted tests would be the date of testing rather than the date of specimen collection. The OPPS 2018 definition of a qualifying ADLT only refers to criterion A, and does not qualify a test as an ADLT using criteria B or C. The new rule goes into effect with January 1, 2018 date of service. This new rule does not change the inpatient 14-day rule.

How the new rule will impact your revenue cycle depends on the type of testing your lab performs for Medicare hospital outpatients. The biggest change is the opportunity for labs who perform testing excluded from the OPPS packaging policy to bill Medicare directly, using the date of testing as the date of service on the claim.

How will this impact your lab’s reimbursement? Hospitals who have been administratively and financially burdened by the outpatient 14-day rule, may be incented to withdraw from institutional billing arrangements in favor of the lab billing Medicare directly. Consider the following.

- If your lab test is covered by Medicare, is the allowed amount listed on the Medicare CLFS more or less than your current institutional billing fee schedule? How will your lab address and process Medicare pre-claim requirements such as medical necessity or local coverage determinations? Does your claims clearinghouse check for Medically Unlikely Edits (MUEs)? When exposed to MUEs, will your claims submission process perform the necessary edits to ensure your Medicare claims make it to adjudication?

- If your test is not covered by Medicare, or Medicare’s reimbursement is not at an acceptable level, you may want to attempt to retain the current institutional billing arrangement—such an arrangement is not precluded by the new rule. Ensure your billing system can report the appropriate DOS on the institutional invoice for the ADLTs and molecular pathology tests excluded from OPPS packaging policy. As hospitals have historically absorbed the cost of these tests performed for Medicare hospital outpatients, they may be unwilling to retain institutional arrangements except for those qualifying tests that are in high-demand.

How will the outpatient 14-day rule change affect test ordering behavior? Hospitals waiting to place test orders on day fourteen, can now order tests earlier. Will earlier ordering improve test result quality and delivery? Working with viable specimens, producing better results, and providing faster turnaround times?

The OPPS 2018 laboratory DOS policy exceptions open up a whole new world of reimbursement for labs who perform testing excluded from the OPPS packaging policy. As you consider how these changes will impact your lab’s revenue cycle process and reimbursement results, learn how Quadax can help. Experienced in laboratory revenue cycle optimization, we help labs of all types maximize their revenue.

Living with PAMA–What is Your Lab’s Prognosis?

The financial impact of PAMA to your laboratory depends largely on the type of testing you perform. With the recent publication of the 2018 Medicare CLFS reimbursement rates, it is clear that high-volume clinical laboratory testing is facing substantial downward pricing pressure while much of the advanced molecular diagnostics and genomic testing market reimbursement is neutral to positive. Because of this, it is not surprising that two influential industry groups, the American Clinical Lab Association (ACLA) and Coalition for 21st Century Medicine (C21), have issued opposing statements about the implementation of PAMA. Notwithstanding a successful last-minute legal challenge by those opposing PAMA, the industry must prepare for the likelihood and reality of an implementation on January 1st, 2018. If you haven’t done so already, knowing how PAMA will impact your lab’s revenue is a critical next step in this preparation.

The Protecting Access to Medicare Act of 2014 (PAMA) revised the payment methodology for clinical diagnostic laboratory tests paid under the Medicare Clinical Laboratory Fee Schedule (CLFS). Final Payment rates released November 17, 2017 will be implemented effective January 1, 2018. Studying Medicare’s new market-based payment system for laboratory services, there are areas of opportunity. Preliminary analysis indicates that molecular and genetic diagnostic testing services may benefit from the new rates. Other clinical testing services may experience a decrease in rates, in which case it becomes very important to understand which claim populations are impacted. may need to apply more complex financial models. All laboratories should also consider PAMA’s secondary impact on commercial payers (both contracted and non-contracted) who derive their allowed amounts from the prevailing Medicare CLFS. Trying to determine the exact impact PAMA will have on your lab can be its own challenge.

Quadax has developed a proprietary modeling tool that is helping our laboratory clients plan and prepare for PAMA’s initial and on-going impact. By using this tool to identify and quantify areas of greatest challenge and opportunity, our client service teams provide the data to help drive our customer’s decision-making process. To deliver the best results, we collaborate with our clients bringing together our joint expertise in the analysis and interpretation of the data, reporting requirements, and clinical aspects of the tests. If you are interested in learning more about our proprietary PAMA modeling tool and how we can use it to benefit your lab, please contact us. We are here to help.

As your lab considers future opportunities—from enhanced operating efficiencies to test menu diversification—an optimized revenue cycle management solution is key. One that solves for both tactics and strategy so that reimbursement efforts maximize revenue in the new world of PAMA-driven pricing.

Defining Your Hospital Lab Program’s Value in the Face of PAMA Cuts

In the face of PAMA’s substantial cuts to the Part B Clinical Laboratory Fee Schedule (CLFS) on January 1, 2018, many hospitals are reassessing the value proposition of their laboratory service offering.

Before deciding to sell or outsource portions of your lab program, your health system may want to consider the laboratory’s contribution to an enhanced patient experience and the powerful patient management decision support afforded by mining laboratory data. Though such a decision to divest your laboratory operation may produce short-term benefits, it may limit long-term growth strategies and competitiveness for your health system.

The PAMA Impact

The Protecting Access to Medicare Act of 2014 (PAMA) revised the payment methodology for clinical diagnostic laboratory tests paid under the Medicare Clinical Laboratory Fee Schedule (CLFS). With the implementation of PAMA just months away, hospitals are reevaluating their laboratory business. Just how big an impact will PAMA have on your lab’s revenue? In the context of a hospital lab program’s possible three business segments – inpatient, outpatient, and outreach (e.g. non-hospital patient) – it appears only outpatient and outreach will be affected by PAMA, with the greatest impact on outreach.

- Inpatient lab services, governed by Part A, are not impacted by PAMA cuts targeting Part B. Also, Medicare reimburses hospitals for inpatient lab services as part of Diagnosis Related Group (DRG) bundled payments and therefore does not use the CLFS for payment rates.

- Outpatient lab services, governed by Part B, are most often paid by Medicare within Ambulatory Payment Classifications (APC) payment bundles. Medicare has bundled the majority of CLFS and the technical component of most anatomic pathology procedures from the Physician Fee Schedule (PFS) into the Evaluation and Management (E&M) service payment. However, PAMA rates will still apply to a small subset of CLFS CPT codes that are still paid fee-for-service (e.g. molecular diagnostics).

- Outreach lab services performed on non-hospital patients will be the segment most impacted by PAMA.

Gain Operational Efficiency

Hospitals expect their labs to be efficient, productive, and competitive. Can hospital labs gain the efficiency to offset anticipated losses expected with PAMA? Do they have the right equipment? Are they doing the right tests on site? Are they staffed appropriately and processing specimens in an efficient manner? Are test menus optimized across multiple hospital campuses? Is your lab increasing the number of patients served and tests performed, while decreasing the need to repeat tests through improved specimen handling and result reporting? Operational efficiency benefits from continuous improvement efforts. Track your lab’s success in this area by using key performance indicators (KPIs) such as turnaround time (TAT), count of unresulted or canceled lab tests, reagent and material cost per accession, and labor costs. While operational efficiency is important, defining your lab program’s value still requires a wider view.

Separate Your Lab’s Financials, Claim Management and Reimbursement Processing

A health system’s lab financials are often rolled-up to combine with hospital figures. As part of a merged Profit and Loss, it can be difficult to track the true financial performance of the lab program. The lab’s financial performance can also be impacted by the sharing of hospital billing and reimbursement resources. Viewed as a secondary initiative by shared resources, lab programs may experience a higher incident of bad debt due to inefficient collections and low net revenue. Lab testing services reimbursement efforts may benefit from separation through the implementation of a lab-centric revenue cycle solution.

Another reason to consider separation, is the unique pre-claim requirements of specialized testing. As health systems bring genetic and molecular testing to their hospital lab program to drive personalized medicine, the steps needed to get reimbursed correctly require expert knowledge and processing. Cutting-edge molecular and genetic tests must meet payers’ medical necessity and prior authorization requirements.

Many hospitals now find themselves in a Medicare Administrative Contractor (MAC) Jurisdiction that has implemented the MolDx program. In order to be considered for reimbursement, all Part A and Part B claims for molecular diagnostics testing, whether performed in-house or by a reference laboratory, must be submitted to the MAC with the appropriate Diagnostics Exchange (DEX) Z-Code assigned to the test. Given these and other MolDx billing requirements, your hospital lab program may want to consider laboratory business process outsourcing options to receive maximum reimbursement for specialized testing since many legacy hospital billing systems are unable to adapt to the special billing requirements of the MolDx program. Even for a mid-sized hospital, hundreds of thousands of dollars may be left on the table because of the inability to submit Z-Codes on your claims for molecular diagnostics testing to your MAC.

Alternative Value Proposition

Using cost containment as the sole basis for determining a hospital lab program’s worth may be too limiting. How does your hospital outreach lab contribute to your health system’s patient experience? Balancing service and return-on-investment, health systems may want to consider the value of quality testing done onsite with rapid turnaround times.

What about serving the increasing number of hospital-employed physicians? As physician provider’s become hospital employees, labs are jockeying for position. Hospital labs have a unique advantage… location, location, location. But to leverage that advantage, hospital labs need to sell their service, speed, and quality to the ordering physicians. Is your hospital lab program creating valuable connections with hospital employed physicians? Can your outreach lab compete solely on a cost basis? Or is there additional value to be considered?

Laboratory data is actionable and has predictive value. As hospitals and health systems move toward value-based health care, their lab programs could provide a major source of information. What if your hospital lab was viewed as a collaborative partner offering innovative data analytics, utilization management, and diagnostic decision support? What if your lab could gather information on and provide an understanding of referral patterns, helping physicians order the right tests?

Defining Your Hospital Lab’s Future Value

Many health system executives feel forced to sell off the lab program because it is not viewed as a core fundamental service. Without a process in place to measure the profitability or value of their lab’s business, hospitals tend to undervalue their worth. You can respond by communicating your lab’s value. You can start by optimizing your lab’s revenue cycle. Quadax, an expert in laboratory billing, can help. With service options sized to fit (Business Process Outsourcing, Software-as-a-Service, Hybrid), your lab can maximize reimbursement and demonstrate its value. Learn more about Quadax services, visit Understanding Your Lab’s Revenue Cycle.

Is Your Lab Aware of CMS Claim Requirements for “Unlisted” Test Codes?

Centers for Medicare & Medicaid Services (CMS) released Transmittal 3881 on Friday, Oct. 13, 2017 requiring the submission of data for lab tests processed with “unlisted” codes effective beginning January 16, 2018. Medicare Contractors (MACs) will report to CMS specific laboratory tests and associated claims data for any test paid under the Clinical Laboratory Fee Schedule (CLFS) as a Not Otherwise Classified (NOC), Not Otherwise Specified (NOS), or an Unlisted Service or Procedure code, including but not limited to the following: 81099, 81479, 81599, 84999, 85999, 86849, 86999, 87999, 88749 and 89398. Claims that fail to follow the new procedures will be returned as unprocessable.

Strategies for Managing Genetic and Molecular Test Preauthorization

{kind=link}

In the world before molecular diagnostic CPT codes and payer required prior-authorization, labs could develop, validate, and immediately go to market with a new test. Labs focused their accession workflows on delivering rapid turnaround times and deferring reimbursement efforts until after test results were reported. Today, many payers require pre-test authorization for genetic and molecular tests. Using third party online utilization management programs, payers are able to enforce pre-testing requirements. To secure reimbursement, labs will need to determine how best to integrate prior authorization into their accession and revenue cycle workflows.

Know Your Payer Requirements.

When it comes to preauthorization, it is important to know what your payers require. Some prior authorization programs may require test registration and/or genetic counseling and may limit or discontinue retro-authorization options. The latest payers to adopt such programs are Anthem Blue Cross and UnitedHealthcare.

Define Your Lab’s Financial Goals.

Before you can determine the best strategy for managing pre-test authorization, you need to define your lab’s financial goals and establish your lab’s identity, including the willingness to trade reimbursement for market share and volume. Start by analyzing your historic revenue data. Analytics will help you understand and anticipate what the new pre-test requirements will cost your lab. A good revenue cycle system can help you identify which of your tests, patient populations, providers, and payers perform best financially and which do not. Investigate under-performing product-market segments. Is it a volume issue, a cost issue, or both? Are the right tests being ordered and performed? Engage in a low-cost, high-impact educational campaign targeting providers and patients as well as your own sales team and back-office support.

To Test or Not To Test – Things to Consider.

When you are sure the right tests are being properly ordered, you need to decide whether or not your lab should perform the tests. Delivering rapid turnaround in the midst of rigorous payer pre-test requirements adds complexity and cost to your lab’s operations. What level of calculated risk to reimbursement is your lab willing to accept in order to maintain market share and deliver rapid turnaround? Here are some things to consider during your decision-making process.

- With certain exceptions, Medicare defines Date of Service (DOS) as the date the specimen is collected, making it virtually impossible for the laboratory to obtain prior authorization after the specimen has been received. Some commercial and Medicare Advantage plans may allow the DOS to be the date the test report is signed. It is in the lab’s best interest to have all pre-test requirements before starting the test. Pre-test requirements include not only payer prior authorization, but also basic coverage determination. In the event the test is not a covered benefit, the payer may require patient consent through the use of an Advance Beneficiary Notice (ABN) form in order to bill for the test. How will the need for prior authorization and ABN impact your accession process? Consider deploying a client-facing ordering portal that will include the payer pre-test requirements so that the ordering physician has the necessary information at the time of ordering.

- Another strategy is to revisit your payer contracts. If during payer negotiations your lab cannot eliminate a payer’s requirement for prior authorization, then you may want to attempt to negotiate the terms. Some labs have been successful in negotiating a 2-week window from specimen collection in which to secure pre-test requirements. If granted, it would be the lab’s decision whether or not to go to testing during this time, tailoring accession operations based on product-market segment performance. Specimens from high-performing segments would move to testing immediately, while specimens from other segments could be held until all pre-testing requirements are met.

- Consider the demands of proper specimen handling. Many biological specimens (blood, urine, bone marrow) do not have long viability. Define your lab’s specimen handling requirements to ensure the integrity of your test results. Identify these procedures and protocols in your negotiations with payers stating the adverse effects of testing delays. Plan for these operations in your accession workflow strategies.

Choose Your Next Move.

The choices you make for how your lab moves forward in the midst of today’s rigorous pre-testing requirements depends on your lab’s ability to optimize its revenue cycle while delivering quality test results. Achieve operational success and maximize reimbursement efforts by understanding the payer’s requirements and then deploying an optimized, prioritized workflow.